May 9, 2026

Something Is Off About This Rally

May 2026. New highs, elevated valuations, a Fed that won’t budge, and oil at $114.

The S&P 500 closed at a fresh all-time high of 7,209 in late April — its strongest monthly gain since November 2020. The Nasdaq followed. And yet Brent crude is sitting near $114–$120 a barrel, the Fed hasn’t moved rates in months, and the U.S.-Iran conflict is still very much a live variable. None of that stopped the rally. So either the market knows something, or it’s choosing not to look.

Here’s where I’m at: the earnings picture is genuinely strong. Q1 blended year-over-year growth came in around 15.1%, up from the 13.1% expectation heading into the season. That’s not a rounding error — that’s six consecutive quarters of double-digit earnings expansion. Hard to argue with that. But the forward P/E on the S&P 500 is now sitting near 20.9x, above both the five-year average of 19.9x and the ten-year average of 18.9x. The index is being priced for this trajectory to continue, not slow.

That’s the tension. And it’s not going away anytime soon.

Louis Navellier: Don’t buy OR sell another AI stock…

Until you’ve heard this urgent AI warning from the man who called Nvidia before its 44,000% rise…

According to Louis, a massive reset is coming in an obscure corner of the AI market.

This $100 trillion disruption could send some of the world’s biggest AI stocks to zero… and one off-the-radar stock soaring… starting now.

Where the money is actually moving

AI infrastructure is still the dominant theme — and probably will be for a while longer. Microsoft posted Q3 FY2026 revenue of $70.1 billion, up 15.3% year-over-year, with Azure growth accelerating to 33% against a 29% consensus. Operating margins came in at 46.2%. The stock trades around 31x forward earnings, a slight premium to its five-year average. Institutional flows remain net positive given the earnings revision cycle supporting the multiple. That’s the math.

Nvidia is the one everyone is watching heading into late May earnings. Consensus revenue is around $43.2 billion — implying roughly 95% year-over-year growth — with data center expected to make up over 88% of total sales. The stock is near $1,085 on a forward P/E of approximately 34x. Demanding, yes. But the key question isn’t the multiple — it’s whether forward guidance on Blackwell demand exceeds what the buy side already has modeled. That gap is what matters.

AMD is the quieter one worth keeping an eye on. Trading near $148, around 24x forward, with data center revenue up 57% in Q1. It’s underperformed Nvidia by roughly 38 percentage points over the past 12 months. That valuation gap is real, and institutional investors are aware of it. Whether mean-reversion actually materializes depends on Nvidia’s forward commentary more than AMD’s own results — which is a slightly uncomfortable position for AMD holders.

Slight tangent, but it matters: the semiconductor story isn’t just about chips anymore. Taiwan Semi reported April 2026 consolidated revenue up 17.5% year-over-year. The underlying demand signal is consistent. That’s a useful cross-check when evaluating whether Nvidia’s demand story holds.

Your Free Options Book Is About to Vanish

In case you missed it… make sure you get your free “Simple Options Trading For Beginners” book before your link expires.

I eventually plan to charge money for this training, so do yourself a favor and download it now…

That way, no matter what it costs in the future, you’ll have a free copy.

Sound good?

The energy and power infrastructure trade is more interesting than most people are treating it. U.S. electricity demand is projected to grow 15–20% cumulatively through 2030, driven almost entirely by data center buildout and manufacturing re-shoring. Vistra Corp has been one of the top-performing S&P 500 names over the past 18 months — up over 210% from its 2024 lows — and still trades at roughly 11.2x forward EV/EBITDA, a discount to regulated utility peers. Q1 2026 adjusted EBITDA came in at $1.38 billion, up 44% year-over-year.

GE Vernova is the one that doesn’t get enough attention relative to its order backlog. $116 billion — a record. Gas turbines for data center co-location are driving margin expansion toward a targeted 10%+ EBITDA margin by 2027. The stock trades near $378, with street consensus price targets clustering around $418.

Defense and healthcare — the parts people skip

Defense spending is in a structural uptrend. European defense budgets are expected to collectively exceed $430 billion in 2026. The U.S. FY2027 request is $1.01 trillion. These aren’t one-year spending decisions — they’re multi-year commitment cycles that feed directly into backlogs.

RTX Corporation — trading near $128, roughly 20.5x forward earnings — reported Q1 2026 revenue of $20.3 billion with 8% organic growth and a $217 billion backlog. That’s what quality looks like in this environment. Palantir is the more complicated one. Q1 revenue of $884 million, up 38% year-over-year, with U.S. government revenue growing 45% and U.S. commercial revenue accelerating 71%. But at 28x forward price-to-sales, the valuation risk is real. Rule of 40 score of 68 is genuinely strong. The price you pay for that strength is just high.

On the pharma side: Eli Lilly reported Q1 2026 revenue of $13.1 billion, up 45% year-over-year, with tirzepatide (Mounjaro/Zepbound) contributing $5.8 billion of that. Full-year guidance is $58–$61 billion. The stock is near $815, trading at roughly 33x forward earnings — compression from the 45x+ levels in 2024, which is what happens when a theme matures and competition enters. Novo Nordisk is the debate: down roughly 42% from its 2024 peak, now trading near 17x forward earnings on U.S. ADRs. That’s either a large-cap value opportunity or a value trap, depending on how you read the competitive dynamics. Institutions are split.

What the levels say

The VIX compressed hard off April’s peak of 28.6, now sitting near 17.3. Historically, sub-18 VIX correlates with institutional willingness to add risk. But the speed of that compression is worth noting — markets that recover this fast tend to price out risks before they’ve fully resolved, not after. The put-to-call ratio on SPY has normalized to 0.87. Defensive hedging has unwound significantly. That’s fine until a macro catalyst surprises.

At the index level, the S&P 500’s 50-day moving average is near 5,720, with the 200-day at approximately 5,530. Both are meaningful support zones if the index pulls back. Breadth looks okay — the NYSE Advance-Decline line made new 60-day highs recently. That’s constructive. But it also means most of the easy recovery has already happened.

On individual names: Nvidia is consolidating between $1,040 and $1,120 on declining volume ahead of earnings — a coiling pattern that typically precedes a directional move. AMD has built a base between $138 and $152. GEV is in a defined uptrend above its 20-week moving average near $340. Palantir’s critical support sits between $36 and $38 — a break below $36 would signal speculative momentum capital exiting the name.

Three scenarios worth modeling for the rest of Q2. In the bull case — maybe 35% probability — Nvidia’s late-May guidance comes in above $46 billion for Q2 FY2027 (consensus is $44.8B), the Fed signals a June cut on softer CPI data, and the S&P 500 pushes toward 6,100–6,200. AI infrastructure and power names extend leadership. In the base case — call it 45% — Nvidia meets but doesn’t exceed expectations, the Fed holds through July, and the index oscillates in a 5,700–5,980 range. AMD and GEV likely outperform on a relative basis. The bear case — 20% — is simple: core CPI re-accelerates above 3.2%, Nvidia disappoints on demand deceleration signals, the 10-year spikes toward 4.80%, and the S&P 500 breaks below 5,530. Systematic de-risking takes it toward 5,200–5,300. Palantir breaks $36. Lilly tests $740.

What’s interesting is that after a rally this strong — one that ranked as the 25th best month in 1,167 months of market history — the institutional consensus is quietly acknowledging a pullback is more likely than not in the near term. That doesn’t mean selling everything. It means knowing your levels before you need them.

Key dates remaining in May: CPI on the 13th (consensus 2.9% core YoY), retail sales on the 15th, Nvidia earnings estimated around May 28. Those three events will define the rest of the quarter more than anything else.

The most dangerous thing right now isn’t holding the wrong stocks. It’s holding the right ones without knowing why — or without a plan for when they move against you. The market can stay irrational longer than most people expect. It can also resolve faster than anyone’s prepared for.

The numbers above are the starting point. What you do with them is a different conversation.

A note from Media Pub

Right now, robots run the market.

As of 2019, 80% of all stock trading was done by high-efficiency algorithms and bots. That number has since increased.

Wall Street is already letting unemotional, ruthless robots do their dirty work.

So why should you and I be left behind?

This is exactly why I developed K.I.R.A..

The advanced AI engine is designed to outclass any other tool you’ll find out there.

It goes without saying, of course, that K.I.R.A. won’t execute trades on your behalf.

However, it will hand you every single detail you need to take the trade yourself.

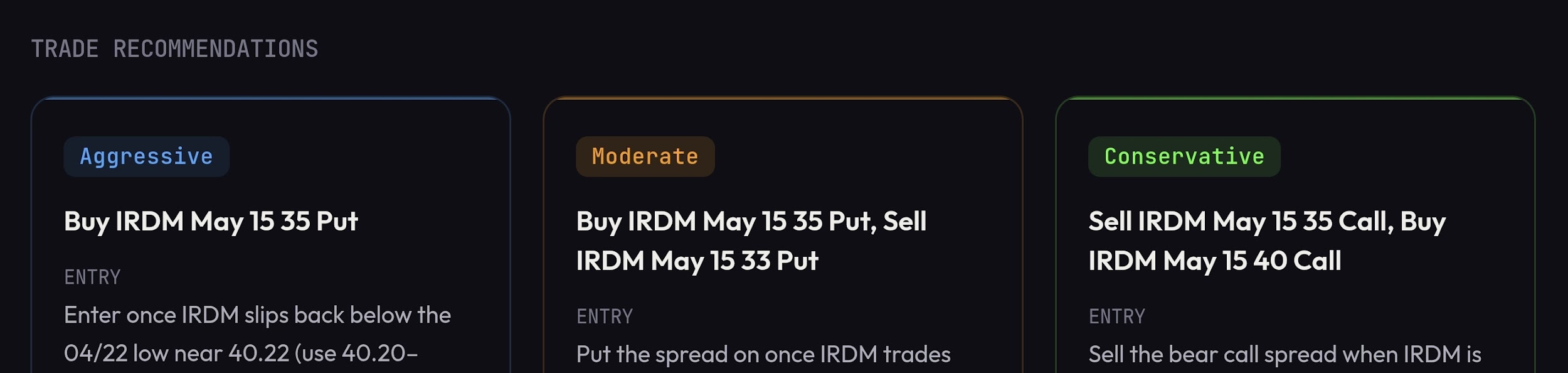

In fact, it isolates three different approaches to the same trade for you to choose from based on how much risk you’re willing to take on.

Now you don’t have to take my word for it.

You can fire K.I.R.A. up right now and see everything for yourself.

Till the next trade,

Lance Ippolito

For informational and educational purposes only. Not investment advice. Trading involves risk, including loss of principal.