June 28, 2026

The Consumer Debt Number Wall Street Is Explaining Away

Auto loans just hit a delinquency record. The gap with stocks is getting harder to ignore.

The stock market is near all-time highs. Consumer sentiment is near all-time lows. And underneath the surface, a consumer debt story is building that the market keeps choosing to contextualize rather than confront.

Here is what the data actually says.

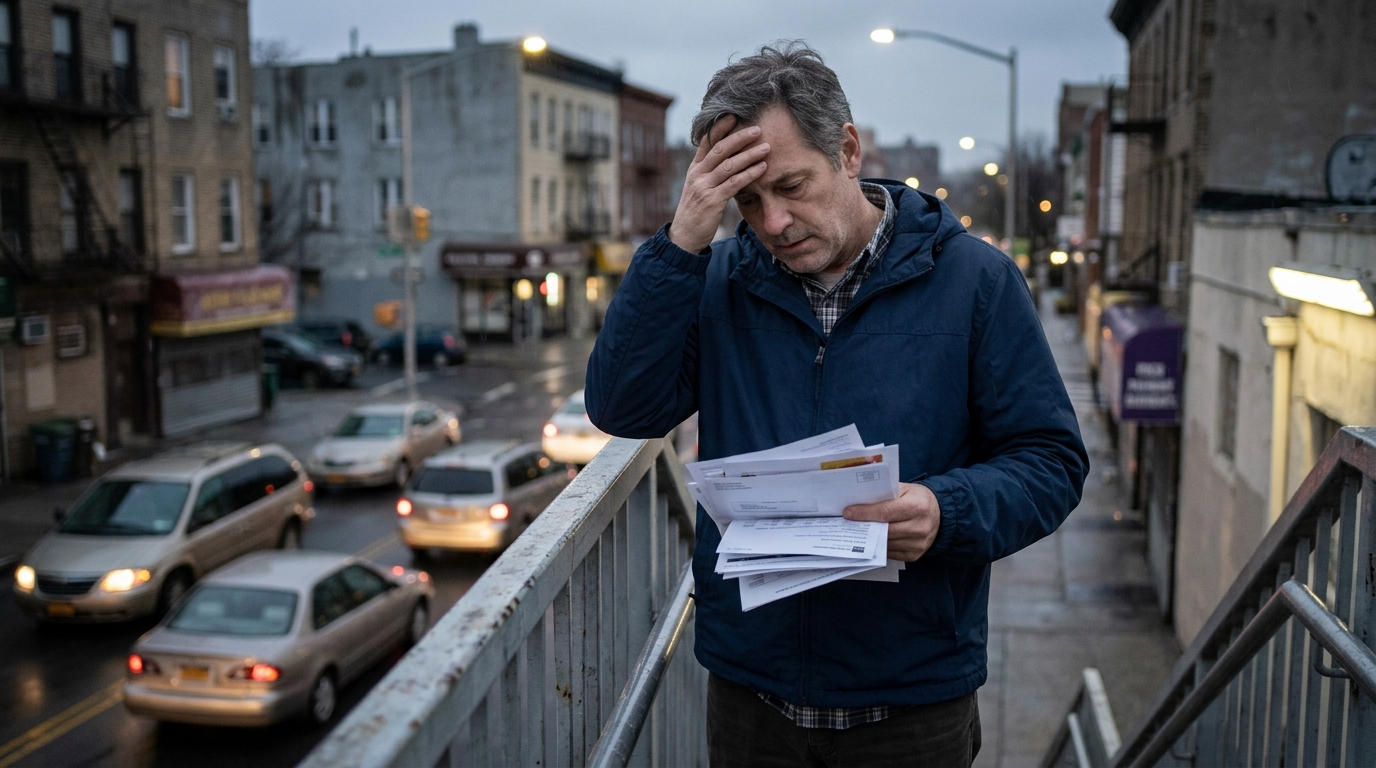

The Numbers

The Federal Reserve Bank of New York’s Q1 2026 household debt report was not a minor update. Total household debt rose to $18.8 trillion. Credit card balances came in at $1.25 trillion, down slightly from the all-time high of $1.28 trillion set in Q4 2025 — though still up nearly 6% from a year earlier. And roughly 13% of credit card balances are now 90 or more days delinquent — the highest rate since 2011, when the country was still crawling out of the Great Recession.

The auto loan picture is worse. The share of auto loan debt that is 90 or more days delinquent reached 5.6% in Q1 2026 — the highest rate ever recorded by the New York Fed, surpassing the prior peak of 5.3% set back in Q4 2010.

Student loan delinquency climbed to 10.3%, up from 9.6% the quarter before, as the COVID-era payment pause fades further into the rearview. Average credit card interest rates sit at 21.52% for accounts carrying a balance. That is the environment in which all of this is playing out.

Market Crash Warning for July 29th

This AI Black Paper is making the rounds on the internet.

And it’s easy to see why. Because if this former CIA advisor is right…

It means – as soon as July 29th – we could see an 80% drop in the Dow.

And it’s going to start with the massive bubble popping in AI.

If you have money in the markets or assets you need to protect…

I suggest you view this message and move your money NOW.

Because once this crisis hits, I doubt you’ll get any second chances.

The Counter-Argument (and Why It Has a Point)

Here is where it gets genuinely complicated.

The stress is not evenly distributed. JPMorgan’s credit card delinquency rate sits at 2.3%. Synchrony’s is 4.8%. That 250-basis-point gap is wider than at any point since 2010, and it tells you something important: the pain is concentrated in lower-prime and retail-card segments, not the prime-borrower base that drives most consumer spending.

Overall household debt service as a percentage of disposable income is still below pre-pandemic levels. And the New York Fed’s own researchers noted that delinquent and newly defaulted student loan borrowers represent only about 2% of the credit population — limiting direct spillover into broader credit markets. The mortgage book is clean. Systemic risk is not the story here.

So the bulls have a point. This is not 2008.

What the Market Is Missing

The issue is not a financial crisis. The issue is demand.

A small but expanding group of consumers has become trapped in credit card debt at 21% interest rates with no obvious exit. Credit experts describe it not as new borrowers falling behind but as those already in delinquency sinking deeper. That cohort will cut spending, not grow it. And consumer spending is roughly 70% of U.S. GDP.

Slight tangent, but it matters: the Philadelphia Fed published research this spring noting that the record auto delinquency rate is partly being driven by an accumulation of borrowers stuck in long-term delinquency rather than a fresh wave of new defaults. That distinction matters for how you read the headline — but it does not make those consumers any more likely to buy a new car or book a vacation.

Travel companies are already seeing consumers trade down from international vacations toward domestic and budget-conscious options. Savings levels have declined. The consumer is not the same consumer that drove the post-pandemic spending surge. That version was running on stimulus, suppressed rates, and excess savings. Those buffers are gone.

Your Free Options Book Is About to Vanish

In case you missed it… make sure you get your free “Simple Options Trading For Beginners” book before your link expires.

I eventually plan to charge money for this training, so do yourself a favor and download it now…

That way, no matter what it costs in the future, you’ll have a free copy.

Sound good?

Who Loses, Who Wins

The clearest losers are consumer-facing companies with lower-income customer exposure. Synchrony Financial and Capital One carry the most visible credit risk in the card sector. Discount retailers serving the lower-income consumer face a buyer who is increasingly cash-constrained.

The less obvious winner is the quality end of the credit spectrum. Prime borrowers are still spending. That benefits companies serving the upper-middle income consumer more than those serving the stressed lower-income segment.

It is also worth watching regional bank earnings closely going into Q2. Small banks carry disproportionate subprime card exposure. Their charge-off rates will tell you more about where this is going than any aggregate headline figure.

The market’s comfort with this data right now assumes the stress stays contained. That assumption may be correct. But it is still an assumption — and it is worth knowing you are making it.