May 1, 2026

TEAM’s Grand Slam

From AI disruption victim to AI monetization proof — in one quarter

Nobody had this on their calendar.

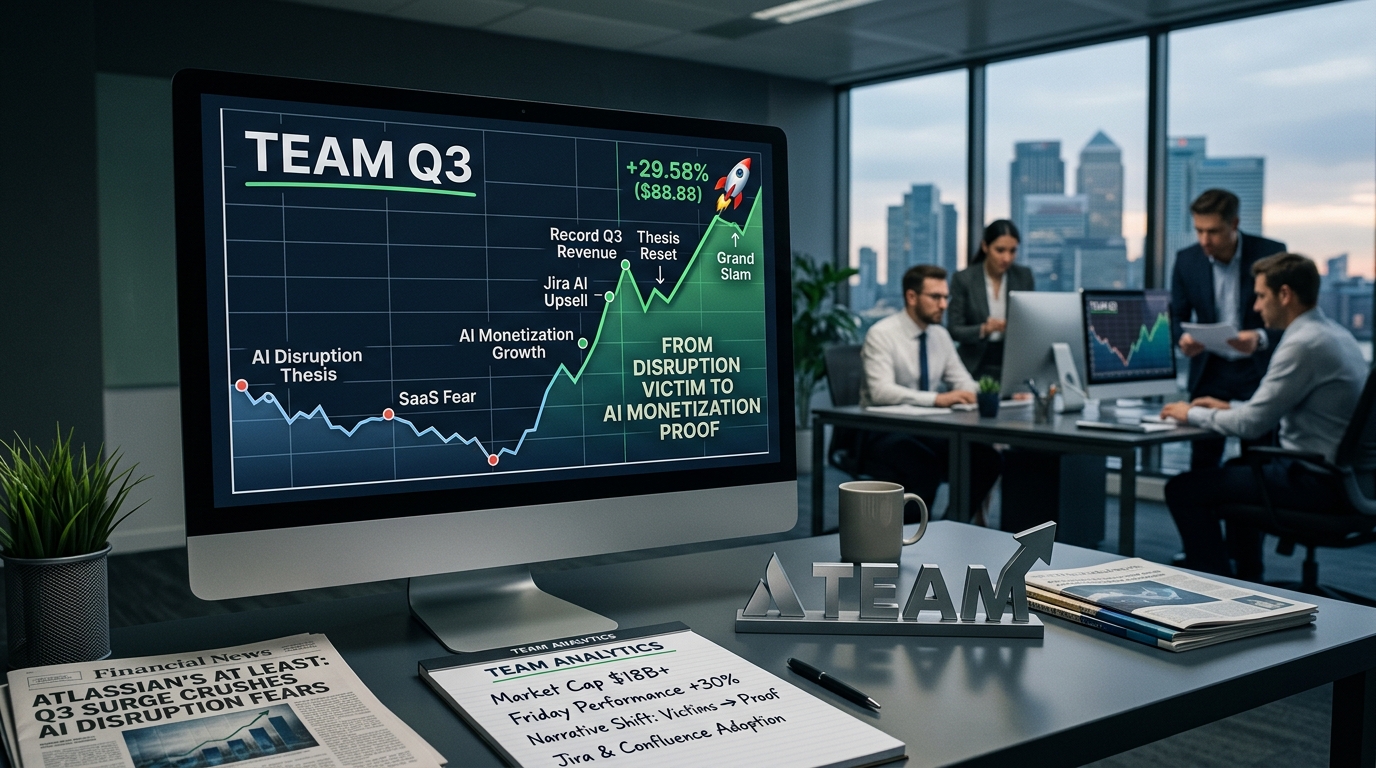

Atlassian (TEAM) closed Friday up 29.58% at $88.88. One session. A near-30% single-day move in a $18B+ software name isn’t a beat-and-raise story — it’s a narrative reset. The kind where a thesis the entire market agreed on gets cracked open by cold, hard numbers. In this case, the thesis was simple: AI is eating SaaS companies alive, and Atlassian is next.

That thesis isn’t dead. But Thursday night’s print put a serious dent in it.

The Setup Before the Print

Atlassian shares had lost about 56.5% since the beginning of the year — a brutal drawdown that reflected genuine fear, not just sentiment noise. The market had priced in existential risk: that AI coding tools and autonomous agents would hollow out demand for Atlassian’s Jira, Confluence, and service management suite. It wasn’t an irrational read. It just turned out to be incomplete.

What the bears missed — and what Q3 laid bare — is that Atlassian wasn’t sitting still. They were building the monetization layer on top of AI, not running from it.

Elon’s $480 Trillion Currency Masterplan

He’s waited 27 years for this moment. Elon Musk just launched his biggest disruption ever, which could totally reset how millions of people access their money and even pay tax.

What the Numbers Actually Say

For the quarter ended March 31, Atlassian reported revenue of $1.79 billion, up 32% year over year and ahead of analyst estimates of roughly $1.69 billion. That’s not a slight beat — that’s a $100M+ revenue surprise on a single quarter. Adjusted EPS came in at $1.75, against a consensus estimate of $1.31. The EPS surprise clocked in at nearly 34%. Both numbers blowing out in the same report — that’s what a Grand Slam print looks like.

Cloud revenue crossed $1.1 billion and accelerated to 29% growth year over year. And then there’s RPO — remaining performance obligations, normalized for ASC 606 — which came in north of 40% growth. RPO north of 40% is the number people skim past. It shouldn’t be. That’s customers signing multi-year commitments. Forward conviction, not backward revenue recognition. It tells you the demand isn’t a one-quarter pull-forward.

On top of the beat, Atlassian raised its fiscal 2026 total revenue growth forecast to approximately 24%, up from a prior outlook of 22%. A guidance raise on top of a blowout quarter is what flips institutional desks from neutral to active buyers. That’s the mechanical reason the stock gapped the way it did.

The Rovo Signal — This Is the Part That Matters

If one data point shifts the AI disruption narrative, it’s this one.

Atlassian’s AI assistant, Rovo, is adding millions of monthly active users with AI credit usage growing more than 20% month over month. That’s already interesting. What makes it a real business story is the ARR effect: customers using Rovo are growing their annual recurring revenue at roughly two times the rate of customers who aren’t. Two times. That means every Rovo adoption is an upsell vector, not a churn risk. The AI integration isn’t hollowing out the product — it’s deepening the customer relationship and expanding wallet share.

Slight tangent, but it matters here: this is structurally different from what the bears were modeling. The disruption thesis assumed AI tools would give customers a reason to consolidate or abandon Atlassian’s suite. The Rovo data suggests the opposite dynamic — customers who adopt AI within the platform become stickier, not looser. That’s a very different business trajectory.

The company’s Service Management Collection crossed $1 billion in annual recurring revenue and is growing north of 30% annually. The Teamwork Collection — a bundled set of applications — is emerging as a significant growth engine as customers upgrade tiers to secure more AI credits. Bundling + AI credits + ARR expansion is a clean monetization loop. It’s not complicated. It’s just executing.

Have You Heard of “Gold Skimming”?

It’s not mining. It’s not buying gold. And it’s not buying gold stocks.

But this strategy has given one group of traders the chance to collect up to $42,920 from the gold markets.

A guy who’s been skimming gold for years just released a free presentation explaining the whole thing.

Trading Cheat Sheet — TEAM

- Friday Close: $88.88 (+29.58%)

- Catalyst: Fiscal Q3 FY2026 earnings beat + guidance raise

- Revenue: $1.79B vs. ~$1.69B est. (+32% YoY)

- Adj. EPS: $1.75 vs. $1.31 est. (~34% surprise)

- Cloud Revenue: $1.1B+ / +29% YoY — accelerating

- RPO Growth: >40% YoY (normalized) — strongest forward signal in the report

- FY26 Revenue Guidance: ~24% growth (raised from ~22%)

- Rovo AI Credit Usage: +20% month over month — MAUs growing

- Rovo ARR Effect: Rovo users expand ARR ~2x vs. non-users

- Service Mgmt ARR: $1B+ / >30% annual growth

- Near-Term Support: $82–$85 (prior resistance flips support)

- Resistance Zone: $95–$100 (gap fill + psychological level)

- Bull Case Target: $110–$120 on continued AI monetization execution

- Bear Case Risk: Fade to $70–$75 if macro breaks or Rovo growth stalls

- GAAP Net Loss: -$98.4M — path to profitability remains a watch item

- Key Risk: Broader SaaS tape weakness + macro deterioration

What I’m watching over the next two to three weeks: whether TEAM holds the $82–$85 band on any pullback. A 30% gap-up in a stock that was down 56% on the year either becomes the foundation of a real trend change or gets faded back into the range. The RPO data and the Rovo usage curve suggest this isn’t a fluke — but the broader SaaS tape is still shaky, and one bad macro print could test conviction fast.

Co-CEO Mike Cannon-Brookes told CNBC that concerns across enterprise software may be overblown, and pointed to the quarter as evidence that Atlassian is turning AI risk into a distinct advantage through what the company calls the Teamwork Graph — essentially a proprietary context layer built from years of customer workflow data that third-party AI tools can’t easily replicate.

Whether the rest of the SaaS sector follows TEAM’s lead — or whether this stays a company-specific outlier — is the real question heading into summer earnings season. One print doesn’t confirm a sector bottom. But it does change the conversation.

The setup just got a lot more interesting.